In order to get a quick loan with affordable interest rate peer to peer lending is a good option. Peer to peer lending option is getting popular in India because it does not require any mortgage to get a loan and without any financial institution as an intermediary. Peer to peer lending is a marketplace where both the lenders and the borrowers need to get registered in P2P networks or platforms which have got a node from RBI. P2P platform works as a bridge between the lenders and the borrowers in order to facilitate loan with ease.

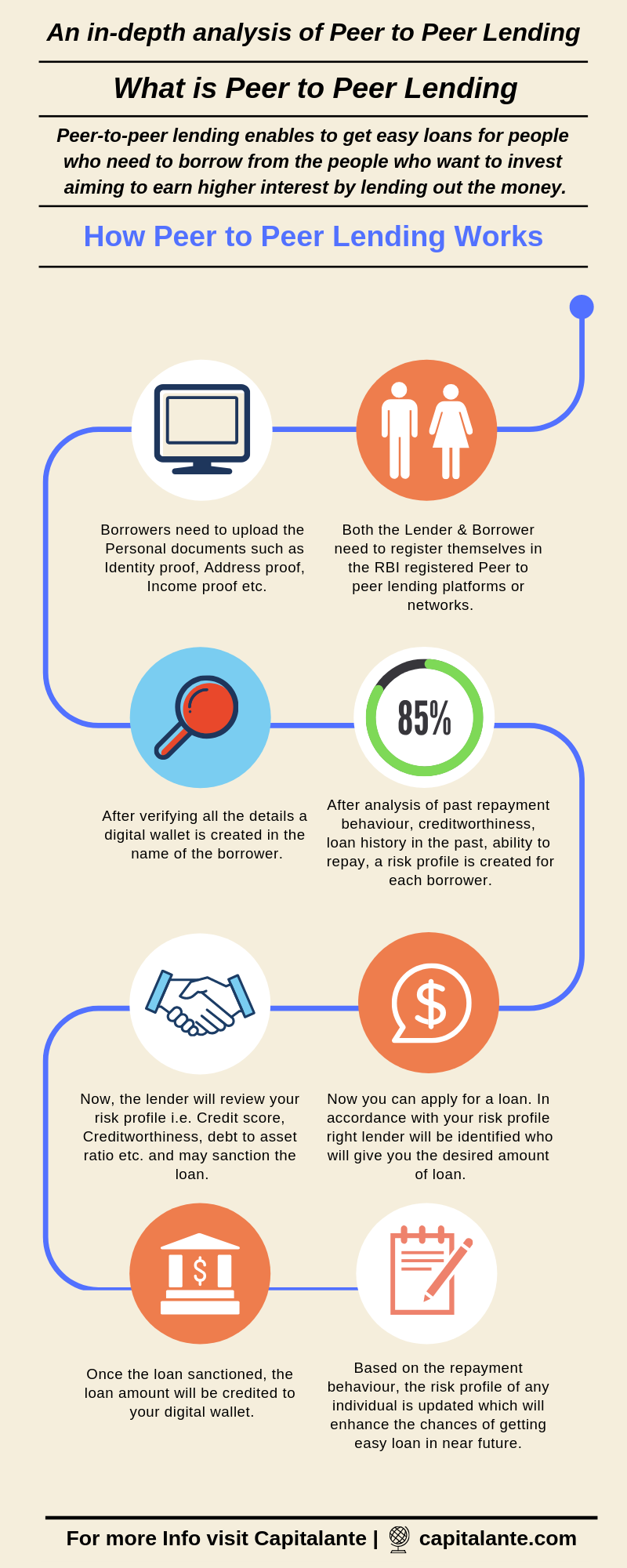

Peer-to-peer lending enables to get easy loans for people who need to borrow from the people who want to invest aiming to earn higher interest by lending out the money. All P2P platforms need to get registered from RBI and RBI has given these P2P platforms a status of non-banking financial companies.

- Read also: Peer-to-peer lending – Wikipedia

How Peer to peer lending works?

Suppose, you require Rs. 100 as a loan. In order to get peer to peer lending, you need to register in any RBI registered P2P lending platform. Now in that P2P platform, there are many lenders available. So, you contact lender Ant and ask for a loan of Rs. 100/-.If you get there the whole amount you do not need to contact any other lender. But if you do not get the desired amount from the lender Ant then you need to contact with the other lenders to get the desired loan of Rs. 100/-.

Let’s make it clear with the help of the following example. Suppose, in this case, the lender Ant agrees to lend you Rs. 20/- only at an interest rate of 12%, so, you get Rs. 20/-. But still, you are short of Rs. 80/- from your desired loan amount of Rs. 100/-. So, you contact several lenders namely Bull, Cat, Duck, Eagle, Fox, Goat etc. Then, among them, Bull, Duck, Eagle, Goat agree to give you a loan of Rs. 20/- each. In this way, you can make use of the P2P platform to get a loan with ease.

How to apply for Loan

There are many RBI registered P2P platforms where any individual need to register for lending as well as borrowing. These platforms are like websites just like any banking websites where you can get a loan or may lend to anyone via online. Any individual can apply for a loan online in these platforms. Whenever your loan is sanctioned by any lender the loan amount will be credited to your bank account.

P2P platforms: Faircent, i2iFunding, Lendbox etc.

Now when the lenders sanction your loan proposal they usually check the following points and after that, they sanction your loan proposal.

- Credit score,

- Creditworthiness i.e. whether you have cleared all the debt amount at a regular fixed interval in the recent past if any,

- Your profile’s debt to asset ratio i.e. the possibility of repayment of a loan by selling your asset whenever required.

The difference between a Business loan from Bank and P2P Lending Platform

In the case of a Business loan from Banks

Usually, there are two types of bank loans available in India namely secured loan and unsecured loan. In case of Secured loans, the borrower has to pledge some assets (such as property, car, shares, debentures etc.) as collateral. But in the case of unsecured loans, the borrower’s assets are not pledged as collateral. The loan is given on the basis of the creditworthiness of the borrower. Let’s make it clear with the help of the following infographics,

In the case of peer to peer lending

One individual is irrespective of the borrower who wants to borrow money and lender who wants to give a loan need to register to create a profile in the online platform to get started. Usually, in the peer to peer lending lenders fix an interest rate and when the borrower accepts the terms and conditions borrower takes loans. Any borrower can see the profile of the lender and vice versa. If the borrower does not get the full amount which he wants to borrow, he can borrow the remaining portion of the loan amount from other lenders also in the P2P marketplace. Let’s have a view of the following infographic.

5 Points to consider while getting started in Peer to Peer Lending Network

Owing to the lucrative returns more than the fixed deposits and mutual funds, peer to peer lending is gaining popularity day by day. It is because the investors i.e. lenders enjoy an interest return as high as 36% per annum. And the borrowers enjoy a less interest rate of 12% in comparison to banks who offer business loan @16-17% interest rate. But in order to get started, you need to consider the following 5 points.

Start Small

Although in accordance with the RBI norms any individual is capped with a maximum amount of Rs. 10 lakh across the entire P2P lending platform, you should invest that huge amount at once. In order to gain double-digit growth do not invest up to the maximum limit. One more thing is to consider if you are earning an interest income of Rs. 50,000/- by lending Rs. 2 Lakhs then you should put the principal back and invest the rest amount in any other asset class to minimize the risk.

You need to diversify

You should diversify i.e. divide your money among various parties. Thus you can mitigate the risk of the default. It is advised if you can bear some risk you can put Rs. 25,000 – Rs. 30,000/- per month to earn up to 36% return annually. You should include at least 100 borrowers in your portfolio if your investment amount is Rs. 1 lakh. Try to control your greed. You may get new borrowers offering more interest rate. But more interest rate carries more risk too. You should evaluate the risk in order to gain a satisfactory return. You may use the formula of 3:6:1. If you have Rs. 100/-, you may invest Rs. 30/- in low risk, Rs. 60/- in moderate risk, and Rs. 10/- in high-risk profiles. You should be sure about the income to debt ratio, CIBIL Score etc. of the borrower before selecting the party.

Always check the borrower’s profile

Select your borrowers and divide them into various categories like very Low risk, Low risk, Moderate risk, High risk, and very High-risk parties. You should evaluate a borrower’s profile and creditworthiness before lending him. Usually, peer to peer companies offers an interest rate between 12.5% and 35% annually on the basis of the level of risk. Many peer to peer platforms give a score out of 100, which determines the risk profile of the borrowers. Usually, a score between 50 and 60 points is considered as a high-risk profile while more than 70 points is considered as a low-risk profile which will attract a lower interest rate. The score is determined by past repayment behaviour, creditworthiness, loan history in the past, ability to repay etc.

Always check the defaulter rate

Defaulter rate reveals the ratio of defaulters in any p2p platform. You should check carefully whether any peer to peer lending platform shows its defaulter rate explicitly on its website. You should choose the older companies to get started.

Tax Implications

In the case of a P2P borrower, one individual needs to deduct TDS on the interest component of the EMI. In the case of a P2P lender the interest earned will be clubbed with the income of the individual under the column of Income from other sources and need to pay tax as per the Income Tax Act, 1961.

- Read also: Top 17 Types of Loan in India

- Read also: What is 50/30/20 Rule of Money

Hope, this article will be helpful for you to get started. If you have any questions feel free to comment so that we can have a discussion. If you have found this post helpful share it with your loved ones.